Fixed Asset Depreciation Rate In Malaysia 2017

Fixed Assets Depreciation Rate Chart Malaysia The Future

Bookkeeping Articles And Resources Accounting For Depreciation

Ar2007 Audited Financial Statements For The Year Ended 30 June 2007

Fixed Assets Depreciation Rate Chart Malaysia The Future

Smeinfo Understanding Tax

4 Ways To Calculate Depreciation On Fixed Assets Wikihow

C that asset was used for the purpose of the business and d at the end of the basis period he was the owner of the asset and the asset was in use.

Fixed asset depreciation rate in malaysia 2017. The next step would be to divide the annual depreciation 1000 with the cost of asset 6000. Rates has been changed for financial year 2017 18 and onwards. 5000 6000 1000 divided by 5. 3 4 person includes a company a body of persons a limited liability partnership.

Depreciation is the systematic allocation of the depreciable amount of an asset over its useful life. Depreciation chart as per income tax act for fy 2012 13 and ay 2013 14 is as under. Blocks of assets are defined based on rates of depreciation of respective block. There are total 13 different rates of depreciation hence there are total 13 blocks of assets.

Depreciation under companies act 2013. The depreciable amount of an asset is the cost of an asset or other amount substituted for cost less its residual value. Now the maximum rate of depreciation is 40. During the computation of gains and profits from profession or business taxpayers are allowed to claim depreciation on assets that were acquired and used in their profession or business.

The annual depreciation would amount to 1000 i e. How to use depreciation rate chart. Calculations must be performed on a quarterly basis. 1 schedule ii 2 see section 123 useful lives to compute depreciation.

03 21731288 printed in malaysia by sp muda printing services sdn bhd 906732 m 82 83 jalan kip 9 taman perindustrian kip kepong 52200 kuala lumpur tel. Hence the annual depreciation rate would be 16 67. The income tax act 1962 has made it mandatory to calculate depreciation. 3 3 resident means resident in malaysia for the basis year for a year of assessment by virtue of sections 7 and 8 of the ita.

Meaning of tax and types of tax in india. Depreciation refers to the decrease in value of an asset over a period of time. While annual allowance is a flat rate given every year based on the original cost of the asset. The person who owns an asset can be the legal or beneficial owner or both.

50706 kuala lumpur malaysia tel.

How To Calculate Depreciation On Air Conditioner

Fixed Assets Depreciation Rate Chart Malaysia The Future

Ausinvestments Economics Finance Investments

Fixed Assets Depreciation Rate Chart Malaysia The Future

Ar2007 Audited Financial Statements For The Year Ended 30 June 2007

Fixed Asset Depreciation Rate In Malaysia 2019

Ar2007 Audited Financial Statements For The Year Ended 30 June 2007

Chapter 7 Capital Allowances Students

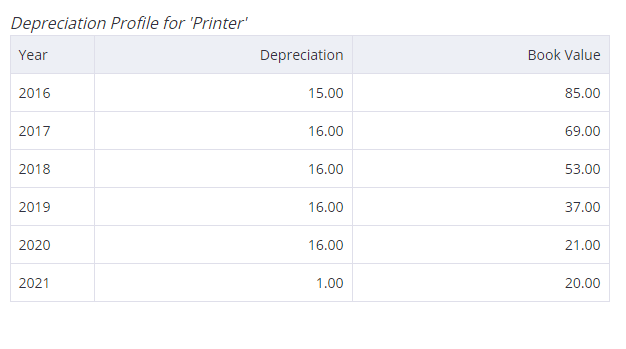

Depreciation Schedule Free Depreciation Excel Template

Http Governanceforstakeholders Com Wp Content Uploads 2018 06 Issues With Wayco Manufacturing 120618 Appendix Pdf

.jpg)

Financing And Leases Tax Treatment Acca Global

Real Property Gains Tax Rpgt In Malaysia 2020

Smeinfo Understanding Tax